China: Acute weakness

implies Global growth is weak, but the authorities don't appear keen to cut

Perhaps explains the weakness of AUD on the crosses - though as my good friend Ben Ashby points out, Australia also has a weak Current Account Deficit AND long positioning

In Andrew Hunt’s latest note, ‘China: Acute weakness’, Andrew highlights the weakness in the Chinese economy; the need for the authorities to ease (but he does not think yet); and he is starting to ease back on his stronger RMB view (which I think would be against the market consensus at this time)

https://www.hunteconomics.com/

If Andrew is correct and the authorities eventually ease policy & the RMB weakens - 1 year 7.00 Digi is circa 7.4% (if nothing happens over the next 6 months, the Digital would be worth 4.75%). CTAs are short USDCNH.

His note

Key Points:

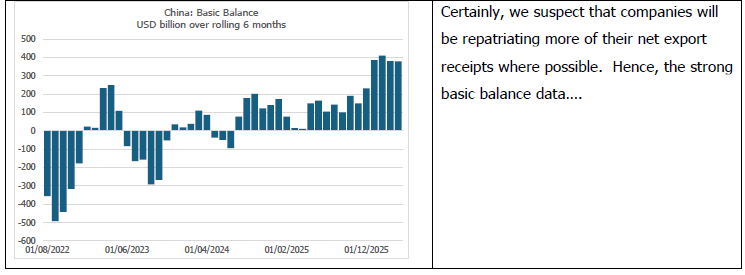

China’s already weak economy has been further impacted by the oil price shock. Economic growth is in reality already minimal / non-existent. This implies that global growth must also be relatively weak now in real terms.

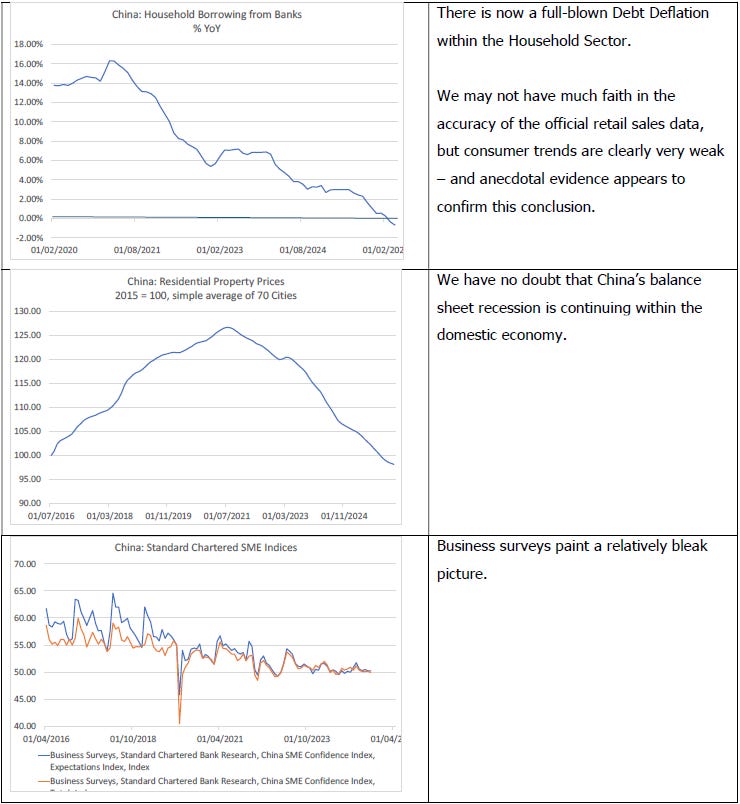

The domestic economy is showing all the hallmarks of a classic debt deflation – rising savings, falling property prices and a weakened domestic financial system

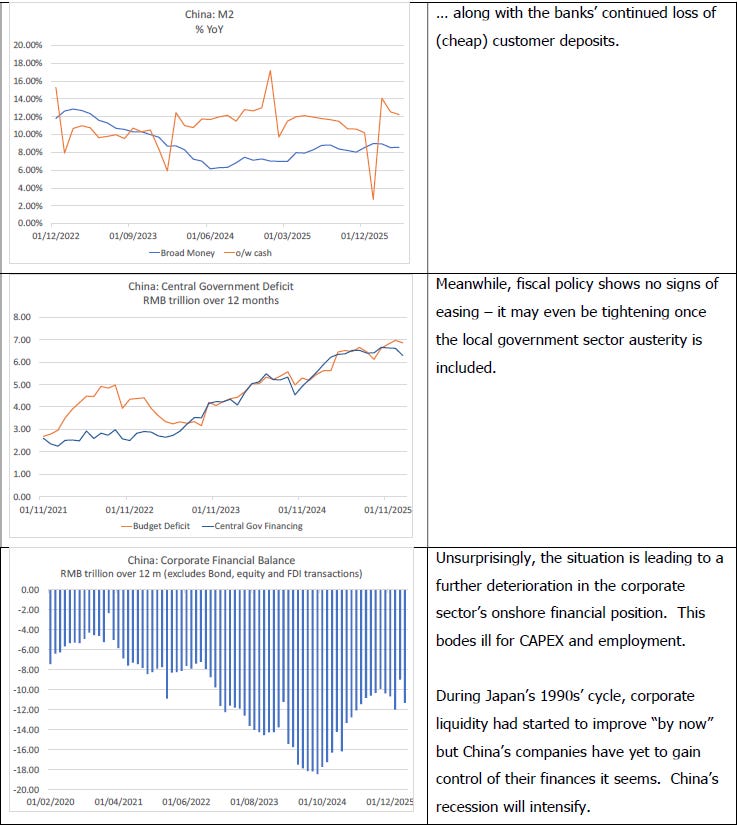

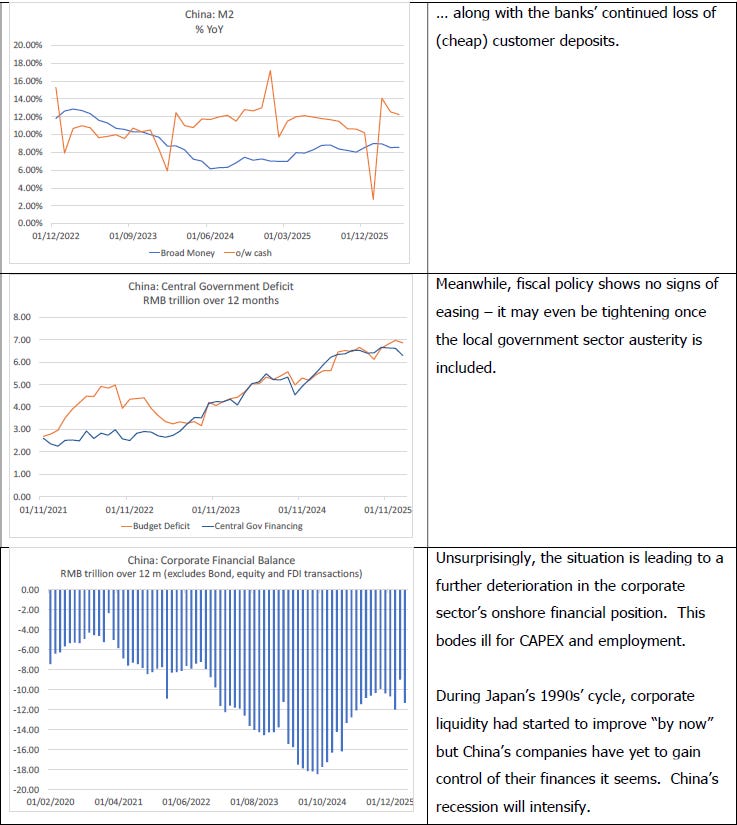

In addition, domestic savers have lost faith in the banks and are continuing to favour cash and alternatives to deposits where they are available. This is increasing the pressure on the already embattled banks.

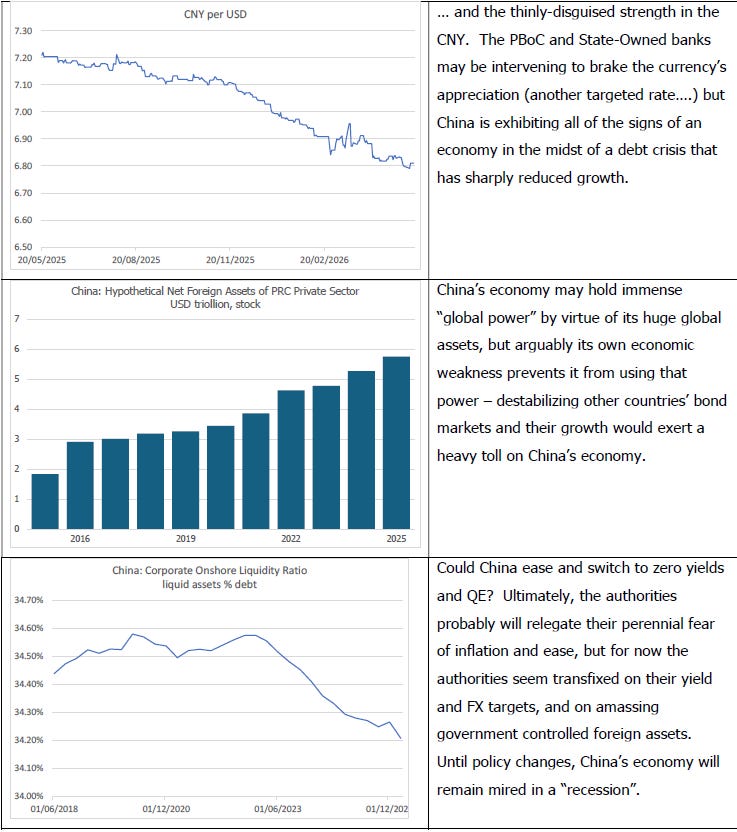

The corporate sector is being sustained by its foreign assets, and the authorities are having to prevent the CNY from appreciating via heavy intervention. We doubt that they would like CNY to appreciate in this environment.

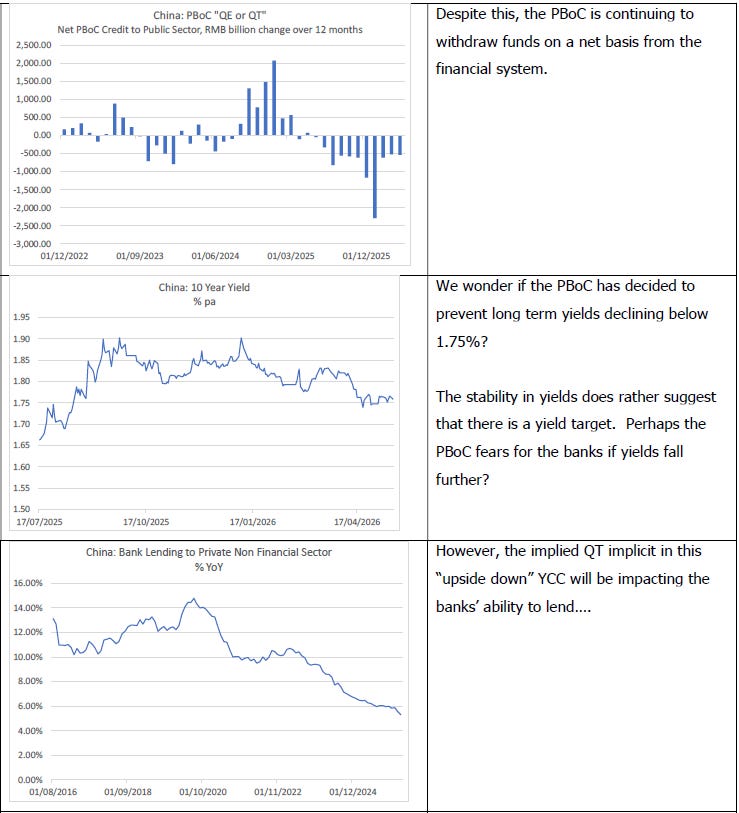

Moreover, Beijing looks to be targeting long term yields at 1.75%, as well as CNYUSD. The intervention in the currency is of some benefit to the system, but the yield target is too high.

Until such time as the authorities mount a U-turn and ease domestic monetary policy settings (despite their fears of a further run on bank deposits and even a rise in structural inflation if they cut rates too far), the economy will remain weak.

When the authorities ease, CNY will likely weaken and yields fall. Although this may not be imminent, we will look to pare back our strong CNY view over the coming months.