Does FX Intervention Suppress Long-Dated FX Implied Volatility?

A market observation, tested empirically

This year, after Japanese intervention in USDJPY, 1Y implied volatility moved lower. A similar pattern appeared after recent RBI intervention in USDINR. Was this coincidence, or do central banks systematically compress long-dated FX volatility after intervening?

• Hypothesis: central-bank FX intervention may create conditional short-vol opportunities

• Test: Japan MoF intervention episodes vs USDJPY 1Y ATMF vol since 1995.

• Result: mixed, but evidence of conditional vol compression.

• Strongest signal appears in larger / higher-vol intervention regimes.

• Follow-up work: RBI (USDINR), SNB (EURCHF), KRW/TWD.

Why this might happen

intervention reduces tail risk

signals policy tolerance

anchors expectations

suppresses realised volatility

How tested

Japan only

Official MoF intervention history

Intervention episodes, not individual days

Sell USDJPY 1Y ATMF volatility at episode start

1m / 3m / 6m / 12m windows

Top-line result: useful, but conditional.

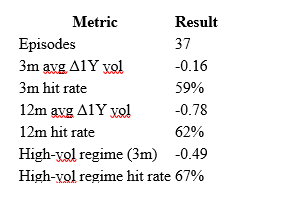

37 tradable MoF episodes since the vol data began

All episodes: 3m 1Y vol change = -0.16 vol pts, hit rate 59%.

12m: average 1Y vol change = -0.78 vol pts, hit rate 62%.

High-vol episodes: 3m = -0.49 vol pts, hit rate 67%.

JPY-weakening interventions worked better than JPY-support episodes in this sample.

The unconditional signal is modest. But intervention episodes in elevated-volatility environments appear to be associated with greater subsequent compression in long-dated implied volatility.

Japan is the cleanest laboratory because intervention history is public and liquid options data are deep. But the more interesting question may be whether the effect is stronger in currencies where intervention explicitly targets volatility suppression — notably India (USDINR) and Switzerland (EURCHF).

That will be the next test.

Results Table

Full workbook available on request / for subscribers.

Methodology note: analysis based on official Japan MoF intervention history and Bloomberg USDJPY 1Y ATMF volatility data (1995–2026). Full event table and workbook available on request.

it has taken some time, but vols lower in USDINR today - lower Oil has helped but the RBI definitely helped stop the rot in INR 3 mth vol at 5.5 from 6 vols last week, and 6.5 during the recent panic, before the RBI stepped in.

{Bloomberg reports that the Indian RBI has sold USD in the FX market to support the rupee. Suspect FX volatility continues to come lower